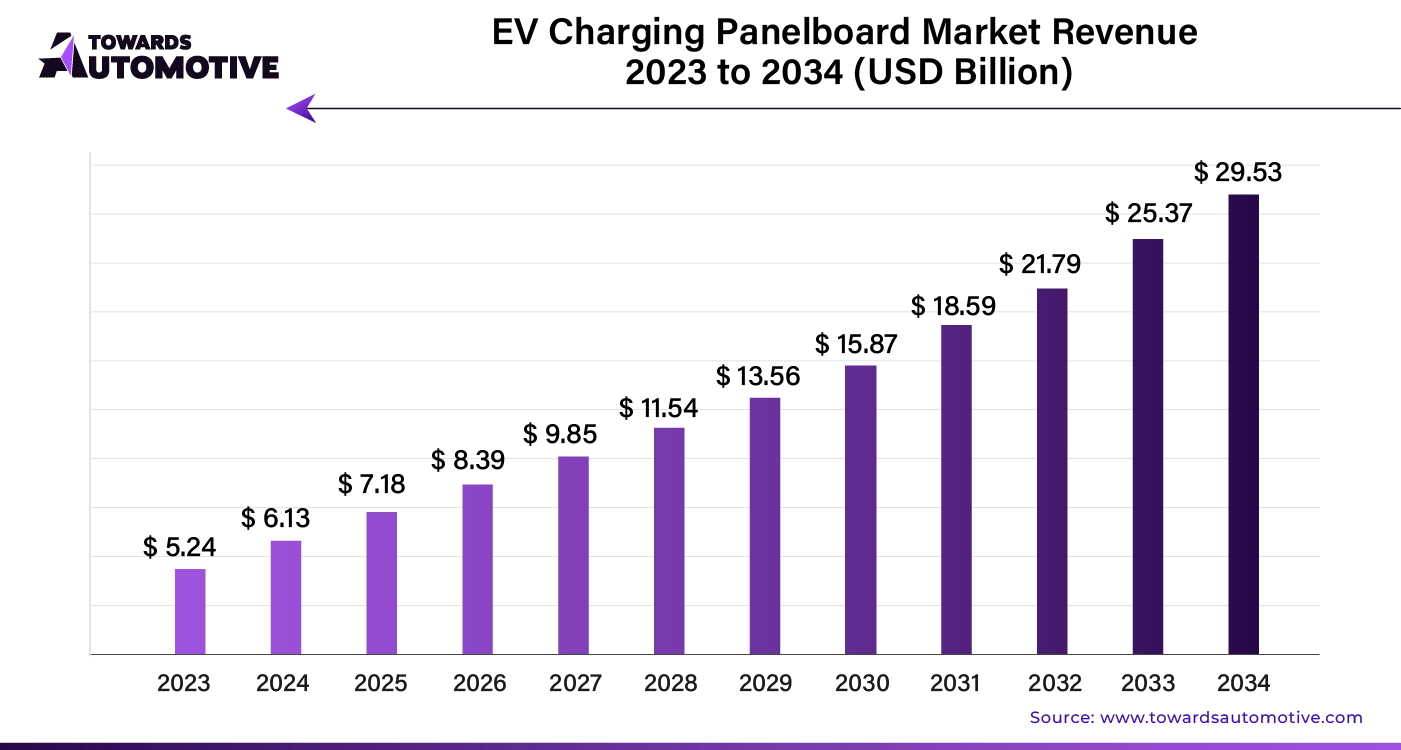

The global electric vehicle (EV) charging panelboard market valued at USD 6.13 billion in 2024, is expected to surge to USD 29.53 billion by 2034, reflecting a robust CAGR of 17.13% over the forecast period.

The rapid expansion of the electric vehicle (EV) market is driving significant demand for EV charging panelboards, a critical component in the infrastructure supporting the shift towards sustainable transportation. As consumers increasingly turn to electric vehicles to reduce carbon emissions and embrace eco-friendly mobility, the need for reliable, efficient charging stations has never been greater, emphasizing the importance of cutting-edge panelboard solutions.

Government initiatives, including subsidies and tax incentives, are further propelling EV adoption and the expansion of charging infrastructure. These policies align with global environmental objectives to decrease greenhouse gas emissions, fostering interest in electric mobility among both consumers and businesses.

The automotive industry, valued at USD 4,070.19 billion in 2023, is on a growth trajectory, expected to exceed USD 6,678.28 billion by 2032 with a CAGR of over 5.66%. This growth, coupled with the continuous evolution of EV charging technology—such as fast charging capabilities and enhanced safety features—underscores the increasing need for advanced panelboards that can support these innovations. The demand for efficient, convenient, and safe charging solutions highlights the essential role of sophisticated panelboards in the burgeoning EV market.

Download a sample version of this report @ https://www.towardsautomotive.com/insight-sample/1360

AI Integration and Supply Chain Optimization Propel Growth in the EV Charging Panelboard Market

AI Revolutionizing the EV Charging Panelboard Market

The integration of Artificial Intelligence (AI) is significantly transforming the EV charging panelboard market, enhancing both efficiency and user experience. AI-driven algorithms optimize the charging process by improving energy distribution, reducing wait times, and predicting peak usage periods to adjust power allocation accordingly. This not only minimizes grid strain but also lowers energy costs.

Predictive maintenance, powered by AI, ensures panelboards remain operational by identifying potential issues before they become critical, thereby reducing downtime and preventing costly repairs. Additionally, AI enhances user interaction with smart features like personalized charging schedules and real-time status updates, further improving convenience for EV owners and boosting overall system efficiency.

Optimizing Supply Chain Efficiency in the EV Charging Panelboard Market

The supply chain is a critical component in the rapidly expanding EV charging panelboard market, ensuring the timely and efficient delivery of products. It encompasses the sourcing of raw materials, manufacturing, and distribution processes. To meet growing demand and technological advancements, companies are investing in robust supply chain management systems that enable real-time tracking, demand forecasting, and inventory optimization.

Effective supply chain management also involves addressing potential disruptions like material shortages or transportation issues. By fostering strategic partnerships and diversifying sources, companies can maintain a steady flow of products, enhancing customer satisfaction and supporting market growth.

East Asia Leads the EV Charging Panelboard Market with Six-Way Configuration Dominance

East Asia’s Market Leadership

East Asia is poised to retain its dominant position in the global EV charging panelboard market, projected to command approximately 50% of the market share by 2024. This leadership is underpinned by several key factors:

-

Surge in Electric Vehicle (EV) Adoption: Countries such as China, Japan, and South Korea are experiencing unprecedented growth in EV sales. This rapid adoption is driving a corresponding increase in demand for EV charging infrastructure, including panelboards. The proliferation of electric vehicles is creating a robust market for advanced charging solutions.

-

Supportive Government Policies: The East Asian region benefits from proactive governmental policies aimed at promoting electric vehicle usage. These include substantial incentives, subsidies, and regulations designed to encourage the adoption of EVs and the development of necessary infrastructure. Such supportive measures not only boost demand but also foster a conducive environment for market expansion.

-

Technological Advancements: East Asia is at the forefront of technological innovation in the EV sector. The region’s ongoing research and development efforts are continually enhancing the efficiency and functionality of EV charging panelboards. Technological advancements are leading to the creation of more sophisticated and effective charging solutions, driving further market growth.

-

Significant Infrastructure Investments: The commitment to expanding and upgrading EV charging networks is a major driver of market growth. East Asian countries are investing heavily in infrastructure development, including the establishment of extensive charging networks. This investment is crucial for supporting the increasing number of electric vehicles and ensuring reliable access to charging facilities.

Dominance of Six-Way Outgoing Configurations

In addition to East Asia’s overall market dominance, the six-way outgoing configuration is anticipated to be a key market leader, accounting for a 22% volume share in 2024. Several factors contribute to this prominence:

-

Expansion of Commercial Charging Infrastructure: The growing need for extensive EV charging setups in commercial and public spaces—such as shopping centers, office buildings, airports, and other high-traffic areas—is driving the demand for panelboards with multiple outgoing circuits. Six-way configurations are particularly well-suited for managing high volumes of charging needs, making them a preferred choice for commercial installations.

-

Fleet Electrification: As businesses and public transport services transition to electric fleets, there is an increasing requirement for charging solutions capable of supporting multiple vehicles simultaneously. Six-way outgoing panelboards are ideal for such applications, facilitating efficient and reliable charging for large-scale operations. This trend is contributing to the higher adoption rates of six-way configurations in the commercial sector.

-

High Demand for Large-Scale Charging Solutions: The need for high-capacity charging infrastructure to accommodate the growing number of electric vehicles is pushing the demand for panelboards with multiple outgoing circuits. Six-way configurations offer the flexibility and capacity required to meet the needs of large-scale and high-traffic charging environments.

Implications for the Market

The dominance of East Asia in the EV charging panelboard market and the growing preference for six-way outgoing configurations highlight the region’s pivotal role in shaping the future of EV charging infrastructure. As the market evolves, continued investment in technology and infrastructure, along with the adoption of advanced panelboard configurations, will be crucial in meeting the expanding demand for efficient and reliable EV charging solutions. This leadership is expected to drive significant growth and innovation in the global EV charging panelboard market.

Forecast and Key Players Driving the Market

The growing adoption of electric vehicles is propelling the demand for EV charging panelboards. Technological advancements, including faster charging rates and smart charging capabilities, are driving the need for sophisticated panelboard solutions. Government incentives and investments in charging infrastructure are also fueling market growth.

Key players like Schneider Electric, Siemens, and ABB are at the forefront, offering advanced panelboard solutions that enhance energy management, safety, and reliability. Companies like Eaton and Legrand further contribute with customized solutions that meet specific regulatory and performance standards, supporting the expansion of EV infrastructure.

Challenges and Opportunities in the EV Charging Panelboard Market

Despite its growth, the market faces challenges such as high initial investment costs and the need for infrastructure standardization. Addressing these barriers is crucial for broader adoption and accessibility of EV charging networks.

Market Insights by Country

Countries like France, the UK, Germany, China, and the US are experiencing robust growth in their EV charging panelboard markets, driven by government incentives, investments in infrastructure, and a commitment to reducing carbon emissions.

Residential Charging Set to Surge

The residential charging segment is expected to lead the market, driven by the convenience and cost advantages of home charging stations. As more consumers adopt electric vehicles, the demand for reliable home charging solutions, including panelboards, is set to grow, supported by government incentives and environmental programs.

Overall, AI integration, supply chain optimization, and strategic investments are driving the EV charging panelboard market towards significant growth, with East Asia leading the charge.

Leading Players in the EV Charging Panelboard Market

ABB Group, Schneider Electric, Siemens AG, Eaton Corporation, Legrand, Leviton Manufacturing Co., Inc., Delta Electronics, General Electric (GE), Mitsubishi Electric Corporation, and Panasonic Corporation dominate the EV charging panelboard market. These top manufacturers and suppliers are actively researching and developing new electrical panels for EV charging stations to meet growing consumer demands.

To enhance their market presence, these companies are pursuing various strategies, including collaborations, mergers, acquisitions, and facility expansions.

Key Market Players:

- Eaton: Offers a range of EV charging panelboards, including the Pow-R-Line Xpert. This panelboard supports up to 10 Green Motion EV smart breaker chargers, featuring revenue-grade metering, remote access, and rapid AC Level 2 charging at 7.7 kW.

- Proteus: Provides comprehensive EV charging circuit solutions for commercial, public, home, and workplace installations. Their range includes custom single and three-phase distribution units, tailored to meet specific client needs.

Top Companies in EV Charging Panelboard Market

- Schneider Electric

- Siemens AG

- Eaton Corporation

- Legrand

- Leviton Manufacturing Co., Inc.

- Delta Electronics

- General Electric (GE)

- Mitsubishi Electric Corporation

- Panasonic Corporation

- Fuji Electric Co., Ltd.

- Electrly

- Enel X

EV Charging Panelboard Market Segmentation

By Outgoing Ways

- Single-way Outgoing

- Two-way Outgoing

- Four-way Outgoing

- Six-way Outgoing

- Eight-way Outgoing

- Twelve-way Outgoing

- Sixteen-way Outgoing

By Location Type

- Residential Charging

- Workplace Charging

- Public Charging

By End-use

- Individual Consumers

- Fleet Operators

- Commercial Entities

By Region

- North America

- Latin America

- Europe

- Asia Pacific

- Middle East & Africa

Get the latest insights on automotive industry segmentation with our Annual Membership @ https://www.towardsautomotive.com/get-an-annual-membership

To own our research study instantly, Click here @ https://www.towardsautomotive.com/price/1360

You can place an order or ask any questions, please feel free to contact us at sales@towardsautomotive.com

For Latest Update Follow Us: https://www.linkedin.com/company/towards-automotive