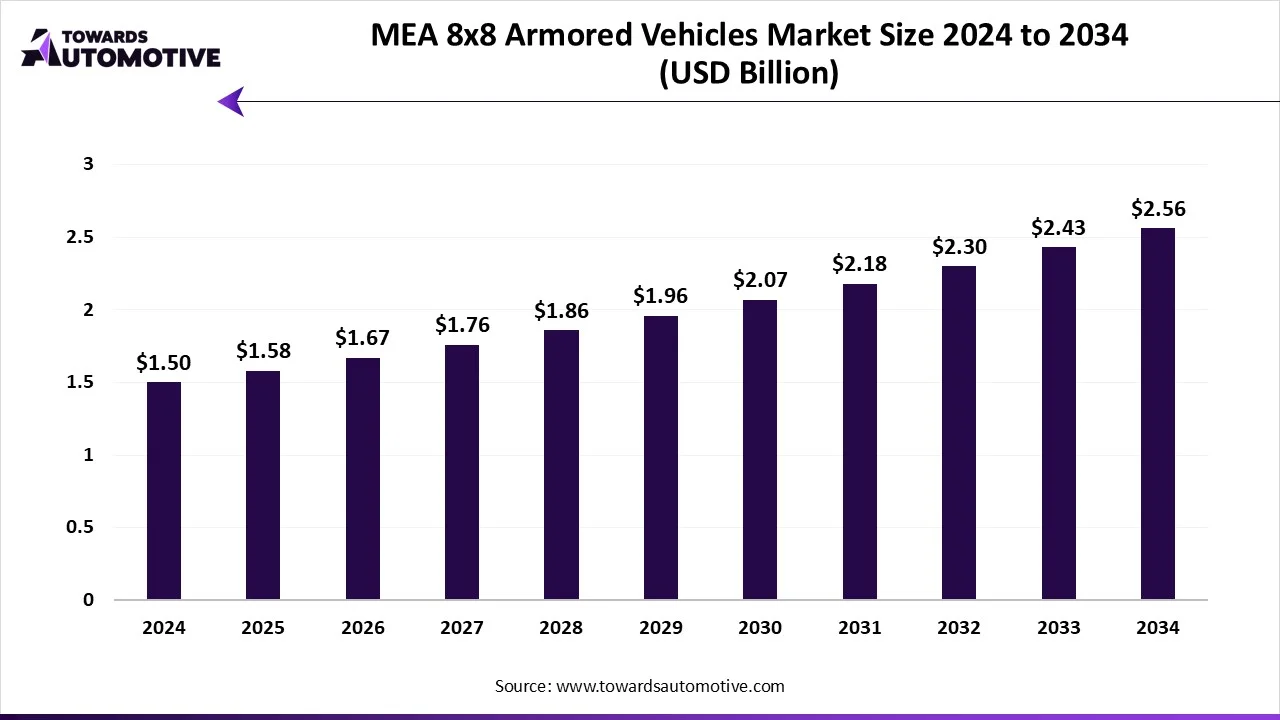

The Middle East and Africa (MEA) 8×8 armored vehicles market is on an upward trajectory, with projections indicating that the market will grow from USD 1.58 billion in 2025 to USD 2.56 billion by 2034, reflecting a compound annual growth rate (CAGR) of 5.5%. This market growth is driven by the increasing demand for advanced 8×8 military vehicles, fueled by the rising geopolitical tensions in the African region and significant defense investments by governments. In addition to these factors, the growing emphasis on technological advancements, including electric-powered 8×8 vehicles, is expected to further bolster market expansion.

The 8×8 armored vehicle is a robust and versatile military vehicle, known for its eight-wheel configuration, and is used for a variety of roles, including personnel transport, surveillance, and combat. These vehicles are powered by different propulsion systems, such as diesel, hybrid-electric, and fully-electric engines. The market is experiencing significant growth due to increasing defense budgets in several countries, particularly in the Gulf Cooperation Council (GCC) nations and sub-Saharan Africa.

Download a Sample of Our Market Intelligence: https://www.towardsautomotive.com/download-sample/1835

Market Dynamics

The MEA 8×8 armored vehicles market is being shaped by various key dynamics, including:

-

Government Investments: Governments in the MEA region, particularly in the GCC, are investing heavily to strengthen their defense sectors. For instance, countries like Qatar are committing around 6.5% of their GDP to enhance military capabilities. These investments are driving the demand for advanced 8×8 armored vehicles.

-

Technological Advancements: The incorporation of cutting-edge technologies in armored vehicles, such as hybrid-electric propulsion systems and advanced armament, has significantly improved the performance and functionality of these vehicles, increasing their appeal in the market.

-

Geopolitical Tensions: The rising geopolitical instability, particularly in the African region, is escalating demand for armored vehicles. Countries are prioritizing the enhancement of their defense capabilities to safeguard their borders and respond to internal conflicts.

-

Partnerships and Collaborations: Key defense players are forming strategic partnerships to develop next-generation armored vehicles. For example, the collaboration between FNSS and SAMI in Saudi Arabia aims to produce advanced 8×8 vehicles tailored to regional defense needs.

-

Electric Vehicles: The trend towards developing electric-powered armored vehicles is gaining momentum, offering improved fuel efficiency, reduced emissions, and lower operational costs, which is appealing to environmentally conscious governments and military agencies.

Key Insights

Geographic Expansion

The Gulf Cooperation Council (GCC) region is projected to hold a dominant share of around 40% in the MEA 8×8 armored vehicles market by 2025. This market share reflects the region’s strong focus on modernizing its defense capabilities through substantial investments in military equipment. Countries such as Saudi Arabia, the UAE, Qatar, and Kuwait have been actively investing in defense infrastructure, recognizing the importance of advanced military vehicles for territorial security, counterterrorism, and internal conflicts.

However, it’s not just the GCC that is experiencing robust growth; sub-Saharan Africa is expected to see the highest growth rate in the coming years, driven by an increasing demand for modern military vehicles. The geopolitical landscape of sub-Saharan Africa, characterized by political instability, armed conflicts, and the rise of militant groups, is fueling the demand for 8×8 armored vehicles. Countries like South Africa, Eritrea, and Guinea have faced escalating security concerns, which has led to increased investments in military technologies and armored vehicles to safeguard national borders and protect civilians from threats.

In particular, African nations are increasingly prioritizing defense modernization programs to bolster internal security forces and enhance their military capabilities. These nations are increasingly looking for vehicles capable of both supporting military operations in rural and rugged terrains and enhancing surveillance in urban conflict zones. Additionally, some of these countries are also seeking international partnerships and collaborations with global defense companies to facilitate the transfer of technology, building local production capabilities to meet the growing demand for armored vehicles.

Vehicle Roles and Missions

In terms of vehicle roles and missions, the Armored Personnel Carrier (APC) segment is expected to dominate the MEA 8×8 armored vehicle market, holding a 32% share. The APCs are designed to transport personnel and equipment safely through potentially hostile environments, making them essential for ground forces in conflict zones. APCs are widely used in warfare and peacekeeping operations, providing protection against small arms fire, explosive devices, and other battlefield threats.

Invest in Our Premium Strategic Solution: https://www.towardsautomotive.com/price/1835

The Infantry Fighting Vehicle (IFV) segment, while smaller in comparison, is expected to experience the highest CAGR in the forecast period. The demand for IFVs has been increasing in the military sector, largely due to their versatility in supporting both combat and surveillance missions. IFVs are equipped with advanced weaponry, armor, and mobility systems, allowing them to carry infantry soldiers into battle while providing heavy fire support. The growing focus on urban warfare, counterinsurgency operations, and border patrols has significantly increased the demand for IFVs, especially in regions facing internal conflicts and external threats. IFVs also play a crucial role in modernizing the defense capabilities of nations, as they are increasingly integrated with advanced surveillance, communications, and targeting systems to meet evolving security challenges.

The trend toward hybrid and electric IFVs has been gaining traction, especially as countries seek to modernize their defense equipment with sustainable solutions. IFVs powered by hybrid-electric systems are expected to offer significant advantages in terms of fuel efficiency, lower emissions, and reduced operational costs, which are especially valuable in regions with harsh environments and logistical challenges.

Protection Levels

The protection level is a critical factor influencing the choice of 8×8 armored vehicles in the market. Currently, the medium protection level (STANAG 3) dominates the market with around 45% of the market share. The STANAG 3 level provides adequate protection against small arms fire, artillery shell fragments, and improvised explosive devices (IEDs), making it a popular choice for a variety of military operations. It is commonly used in peacekeeping missions and low-intensity conflict zones, where the threat level is moderate but still requires vehicles that can withstand certain degrees of ballistic and blast impacts.

On the other hand, the heavy protection level (STANAG 4-5) segment is expected to grow at the fastest rate during the forecast period. These vehicles provide enhanced protection, including armor that can withstand attacks from larger caliber weapons, including anti-tank missiles, RPGs, and artillery shells. As military operations become increasingly complex and involve high-risk scenarios such as urban combat and asymmetric warfare, the need for heavy-protection vehicles that offer superior ballistic and blast resistance is rising. Heavy protection vehicles are particularly favored in regions like the Middle East, where military engagements often involve high-intensity conflicts, and armored vehicles are exposed to greater threats.

Furthermore, many countries are now focusing on integrating next-generation armor systems that combine traditional ballistic armor with composite materials and active protection systems (APS) to counter emerging threats such as guided missiles and drone attacks. These advancements are expected to drive the growth of the STANAG 4-5 segment in the years to come.

Power Sources

Power sources have become a key differentiator in the 8×8 armored vehicles market, particularly as defense agencies seek vehicles with improved fuel efficiency and reduced environmental footprints. Diesel-powered internal combustion engine (ICE) vehicles continue to dominate the market, with a significant share of around 72%. Diesel engines offer numerous advantages, including high torque, reliability, and durability, which are crucial for military operations in demanding environments. Diesel-powered vehicles are also more fuel-efficient and have a better range, making them ideal for extended military operations in remote and challenging terrains.

However, there is a growing shift towards hybrid-electric powertrains in the armored vehicle sector. The hybrid-electric segment is anticipated to expand rapidly over the forecast period due to several compelling factors. The transition to hybrid-electric powertrains offers various benefits, including reduced carbon emissions, lower operational costs, and better fuel efficiency. In regions such as the GCC and sub-Saharan Africa, where environmental concerns are becoming increasingly important, the adoption of hybrid-electric vehicles is seen as an effective way to meet both military and environmental sustainability goals.

Moreover, hybrid-electric systems can improve the operational performance of armored vehicles by providing enhanced energy efficiency and reducing the logistical burden of fuel supply in remote areas. Hybrid-powered vehicles can also benefit from quieter and more stealthy operations, making them suitable for special forces and surveillance missions where discretion is critical. The growing interest in electric 8×8 armored vehicles is expected to further accelerate market growth, especially as electric vehicle technology improves, offering longer ranges, shorter charging times, and better performance in extreme conditions.

Market Segments

The MEA 8×8 armored vehicles market is categorized into several segments, each representing unique characteristics and growth potential:

-

By Vehicle Role / Mission:

-

Armored Personnel Carrier (APC): Holds the largest market share (32%) due to its use in transporting personnel and equipment in high-risk zones.

-

Infantry Fighting Vehicle (IFV): Expected to grow at the highest CAGR, driven by the increasing demand for multi-purpose military vehicles.

-

-

By Protection Level:

-

Medium Protection (STANAG 3): Currently the dominant segment, making up 45% of the market.

-

Heavy Protection (STANAG 4-5): Anticipated to grow with the fastest CAGR as military forces seek greater protection against modern warfare threats.

-

-

By Mobility Capability:

-

High-mobility Off-road: The leading segment, accounting for 40% of the market, favored for operations in rough terrains.

-

Amphibious: Expected to experience the highest growth due to its use in military operations in diverse geographical environments.

-

-

By Power Source:

-

Diesel Internal Combustion Engine (ICE): The dominant power source, holding 72% of the market.

-

Hybrid-electric: Predicted to expand rapidly as the demand for eco-friendly vehicles increases.

-

-

By Weight Class:

-

Medium (12-20t): Holds the largest share at 50%, widely used in peacekeeping and disaster relief operations.

-

Heavy (20-30t): Expected to grow at the fastest rate due to its suitability for carrying large quantities of ammunition and personnel.

-

-

By End-User:

-

Army/Ground Forces: The largest end-user segment, holding a 58% market share.

-

Paramilitary/Internal Security: Predicted to grow at the highest CAGR, reflecting rising security needs in volatile regions.

-

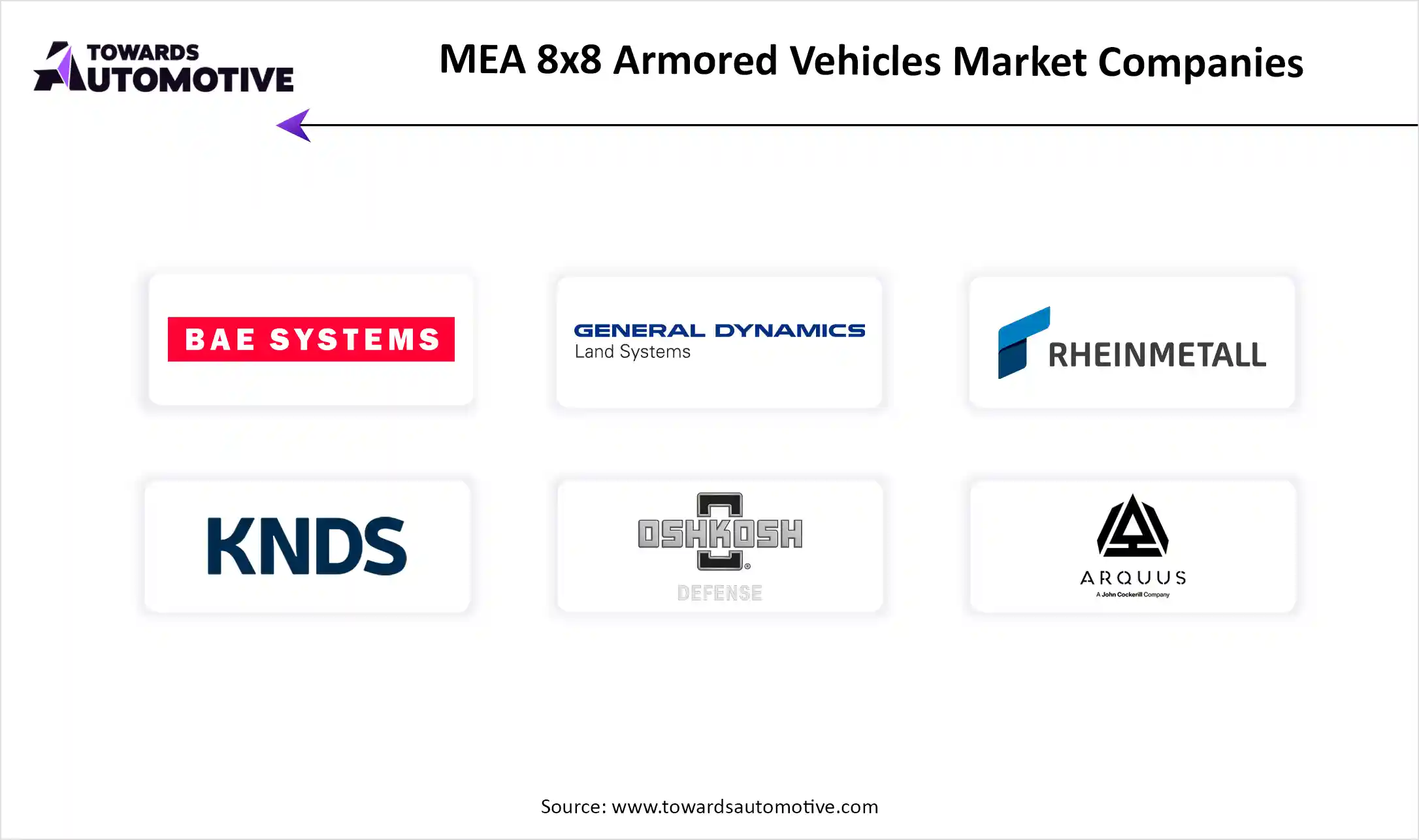

Top Companies in the MEA 8×8 Armored Vehicles Market

1. BAE Systems

-

About: A global defense, aerospace, and security company with a strong presence in armored vehicle manufacturing.

-

Products: Offers a range of military vehicles including the CV90, an advanced infantry fighting vehicle.

-

Market Cap: USD 34.6 billion.

2. General Dynamics Land Systems (GDLS)

-

About: A leading defense contractor specializing in military ground vehicles, including the M1 Abrams tank and various armored vehicle solutions.

-

Products: M2 Bradley Infantry Fighting Vehicle, Stryker Armored Vehicle.

-

Market Cap: USD 52.4 billion.

3. Rheinmetall Landsysteme

-

About: A German defense company known for producing land-based defense systems, including 8×8 armored vehicles.

-

Products: Lynx Infantry Fighting Vehicle, Puma Infantry Fighting Vehicle.

-

Market Cap: EUR 9.2 billion.

4. KNDS (Krauss-Maffei Wegmann + Nexter)

-

About: A joint venture between German and French defense companies, KNDS manufactures a wide range of military vehicles.

-

Products: PzH 2000 Self-Propelled Howitzer, VBCI Infantry Fighting Vehicle.

-

Market Cap: EUR 12.1 billion.

5. Oshkosh Defense

-

About: A U.S.-based company specializing in tactical vehicles for defense applications.

-

Products: MRAP (Mine-Resistant Ambush Protected) vehicles, Joint Light Tactical Vehicle (JLTV).

-

Market Cap: USD 7.3 billion.

FAQs

-

What is driving the growth of the MEA 8×8 armored vehicles market?

-

The growth is driven by increased government investments, rising geopolitical tensions, technological advancements, and the demand for electric-powered vehicles.

-

-

Which region is expected to experience the highest growth in the MEA 8×8 armored vehicles market?

-

Sub-Saharan Africa is expected to witness the highest CAGR due to increasing military needs and geopolitical instability.

-

-

What are the key vehicle segments in the MEA 8×8 armored vehicles market?

-

The major segments include Armored Personnel Carriers (APC), Infantry Fighting Vehicles (IFV), and high-mobility off-road vehicles.

-

-

What power sources are commonly used in 8×8 armored vehicles?

-

Diesel internal combustion engines are the most commonly used, although hybrid-electric vehicles are gaining traction for their environmental benefits.

-

-

Which companies are leading the MEA 8×8 armored vehicles market?

-

Leading companies include BAE Systems, General Dynamics, Rheinmetall Landsysteme, KNDS, and Oshkosh Defense.

-

Source : https://www.towardsautomotive.com/insights/mea-8×8-armored-vehicles-market-sizing

Access our exclusive, data-rich dashboard dedicated to the respective market built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access Now: https://www.towardspackaging.com/contact-us

Become a Valued Research Partner with Us – Schedule a meeting: https://www.towardspackaging.com/schedule-meeting

Request a Custom Case Study Built Around Your Goals: sales@towardspackaging.com

About Us

Towards Packaging is a global consulting and market intelligence firm specializing in strategic research across key packaging segments including sustainable, flexible, smart, biodegradable, and recycled packaging. We empower businesses with actionable insights, trend analysis, and data-driven strategies. Our experienced consultants use advanced research methodologies to help companies of all sizes navigate market shifts, identify growth opportunities, and stay competitive in the global packaging industry.

Stay Connected with Towards Packaging:

- Find us on Social Platforms: LinkedIn | Twitter | Instagram

- Subscribe to Our Newsletter: Towards Sustainable Packaging

- Visit Towards Packaging for In-depth Market Insights: Towards Packaging

- Read Our Printed Chronicle: Packaging Web Wire

- Get ahead of the trends – follow us for exclusive insights and industry updates:

Pinterest | Medium | Tumblr | Hashnode | Bloglovin | LinkedIn – Packaging Web Wire

- Contact: APAC: +91 9356 9282 04 | Europe: +44 778 256 0738 | North America: +1 8044 4193 44